Retirement planning 101: 5 ways to start investing

By Elizabeth Exline

ŌĆ£When it comes down to it, retirement is about survival.ŌĆØ

This statement from Chris Conway, director of financial wellness at╠²░«╬█┤½├Į, can be taken as inspiring or frightening, depending on your perspective. On one hand, thereŌĆÖs a life-or-death quality to the claim. On the other, it distills an opaque concept (retirement planning) into a clear call to action. If you want to thrive in your golden years, start thinking now about when you want to retire and developing a plan for your retirement savings.

For starters, consider when you can realistically retire based on your income and savings, when you can receive your Social Security retirement benefits and the type of investments that might pay the biggest dividends down the line.╠²

Here, Conway breaks down five ways you can╠²approach retirement planning, no matter when you start or with how much income.

How to get started investing for retirement

As with most big things in life ŌĆö marriage, kids, relocating ŌĆö╠²fear can be a powerful obstacle╠²to facing the facts around retirement planning. But when that fear is rooted in a lack of knowledge, it can also be easier to overcome.

ŌĆ£The biggest hurdles are often not knowing what to do and thinking you donŌĆÖt have enough money to start saving,ŌĆØ Conway explains.

ŌĆ£Investing can feel confusing to people given all the options. And those options could lead to losing money, so that makes retirement planning scary. But there are things you can do to learn more and to choose options that reduce your risks.ŌĆØ

While all investments are not created equal (and while it may be wise to make investments in╠²consultation with a financial professional), there are some reassuring general trends.

ŌĆ£Over the years, your stock value will go down, but it will also go up ŌĆö and over time, it usually averages higher,ŌĆØ Conway explains. She cites the S&PŌĆÖs performance since its inception in the 1920s. (This is outlined in an easy-to-read way in InvestopediaŌĆÖs article,╠²ŌĆ£.ŌĆØ)

That means the╠²sooner you start retirement planning, the better╠²ŌĆö and every dollar counts.

5 retirement savings tips

Ready to start putting your retirement plan into action? Keep these five tips in mind.

This article is not intended to serve as financial advice. All financial decisions, including investments, should be made carefully and potentially with the guidance of a financial planning professional.

1. Starting small can yield mighty returns

Can you save $1,000 a month? How about $40?

If the latter sounds more doable, youŌĆÖre not alone. Conway says many students feel comfortable╠²setting aside $10 a week from their income toward their retirement plan╠²rather than committing to a large monthly sum. And if you think itŌĆÖs not worth it to start small, think again.

ŌĆ£If you save just $10 a week and invest it for 40 years, you could have $275,499 from your contributions of $20,800,ŌĆØ Conway explains.

Her calculations are projections, not gospel truth. But they are rooted in data: On average,╠²stocks have earned slightly more than 10% a year╠²since 1928, according to that same╠²ŌĆ£ŌĆØ article.

Curious how much a different amount could yield?╠²╠²are widely available online, and they allow you to customize your retirement plans.╠²╠²

As for what to invest in, Conway says many start with mutual funds or exchange traded funds, since they offer the holy grail of the financial services world: portfolio diversity.

2. 401(k) plans are popular for a reason (or two)

One way to make your money go further is to get someone else to pitch in with you. In the grown-up world of investments, thatŌĆÖs known as an╠²employer-matching program.

ŌĆ£If you can contribute to a 401(k) or similar retirement plan, you should consider doing this to earn any employer match,ŌĆØ Conway says. This means that when you contribute to your 401(k), your employer does too, up to a certain percentage. According to the small-business 401(k) provider Ubiquity, the typical American company╠².

ThereŌĆÖs a catch, though: Employees donŌĆÖt own those matched contributions until those contributions are fully ŌĆ£vested,ŌĆØ or owned by the employee. Vestment periods depend on the company and can range from one to several years.

Even if your employer doesnŌĆÖt offer a matching program, 401(k) contributions are╠²tax-deferred, which means you lower your taxable income each paycheck.

ŌĆ£You might find that a $50 contribution only changes your paycheck by about $40,ŌĆØ Conway says. (There are online calculators available, too, to figure out what the╠²╠²to your paycheck.)

3. Explore the apps

Proving thereŌĆÖs indeed an app for everything is the robust selection of investment apps out there.

ŌĆ£Most apps will invest in index funds or ETFs,ŌĆØ Conway says. Index funds are mutual funds or exchange traded funds (ETFs) that match or closely align to a financial market index.

As a result, index funds tend to be well diversified and relatively popular.

The best part of an╠²investment app, however, may just be how (ahem) invested you are in what happens. You can control how much to invest and when. Certain apps also offer╠²benefits and conveniences╠²like rounding up on purchases and automatically investing the difference.

4. Make it automatic

If you canŌĆÖt trust yourself to make regular investments, or if you just need some accountability to keep yourself on track, consider╠²automating deposits.

ŌĆ£Have it come╠²directly from your paycheck or your bank account, so you donŌĆÖt even see it,ŌĆØ Conway suggests. ŌĆ£Many employers offer programs to increase your 401(k) contributions each year when you receive a raise.ŌĆØ

This is also a great tip for saving in general.

But how much should you be setting aside? The customary amount is╠²10% to 15% of your income, although thatŌĆÖs not set in stone and will depend on when you start saving. Remember: Something is better than nothing. (See the first tip!)

5. Put yourself first

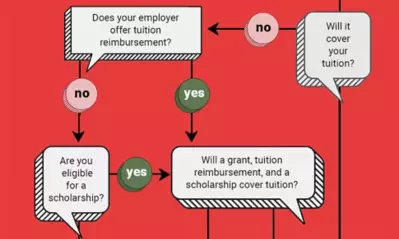

Most adults have a lot of needs competing for their paychecks, especially if they have children. According to Investopedia, the╠²╠²in the U.S. (born in 2017) is $310,605. And thatŌĆÖs just until the kid turns 17!

Saving for a childŌĆÖs college expenses╠²on top of that can seem both onerous and necessary. If it costs that much just for food, clothes, activities and child care, how are you supposed to save for college? And your retirement?

The short answer is: You donŌĆÖt.

ŌĆ£Many financial advisors will suggest you╠²save for your retirement before paying for your childrenŌĆÖs education,ŌĆØ Conway says. ŌĆ£This isnŌĆÖt easy for everyone to accept, especially for older college students who are paying their own way through college!

ŌĆ£This will also be a personal choice, but what you need to consider is why this advice may be sound. Each of us will need to be prepared to╠²financially support ourselves in retirement, and there are no loans or credit available to us to do so. While you may not want to saddle your kids with student loan debt, it is an option that would not exist for you in retirement.ŌĆØ

read similar articles

What is a 529 plan and how does it work?

╠²

Why is it important to invest and save for retirement?

ŌĆ£No one cares about your future more than you!ŌĆØ Conway says. ŌĆ£Social Security alone wonŌĆÖt be enough for most of us to live on in retirement.ŌĆØ

The same may go for basic saving. When you take a dollar and put it in the bank, it remains stable, available and ŌĆö a dollar with little interest added. When you invest that dollar, however, it has the opportunity to grow into much more.

Investing lets you ŌĆ£take advantage of the╠²time value of money,ŌĆØ Conway says. Consider how inflation has decreased the dollarŌĆÖs purchasing power. That dollar in the bank could do more for you if you invest it.

ŌĆ£Investing your money will provide more opportunity to╠²outpace inflation,ŌĆØ Conway explains.

The economy may be out of your direct control, but the date you retire doesnŌĆÖt have to be. Investing for retirement gives you the chance to work your financial situation to your material advantage. YouŌĆÖll thank yourself later.